The Three Basic Letters - IRR

Joseph W. Bartlett, Special Counsel, McCarter & English LLP, Co-Founder of VCExperts

McCarter & English LLP

2002-08-02

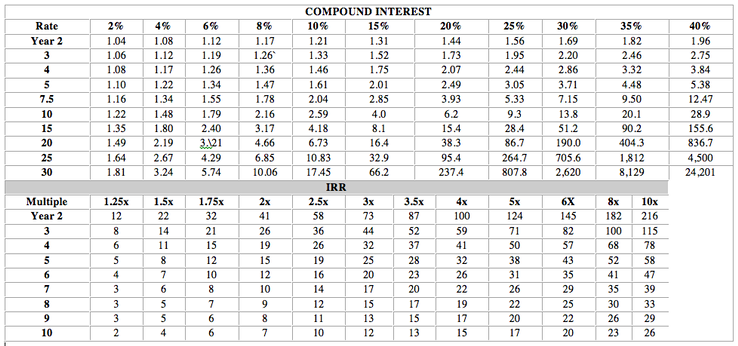

In the old days in this business, returns from harvested investments were calculated quite simply. You put a dollar in–got two dollars back, that's a 100 percent return. Adjust for the time value of money i.e., apply an appropriate discount rate, and you have the answer. In the 70s and 80s, however, the calculations became more sophisticated. The measurement on one's rate of return now takes into account not only the time value of money but also the possibility of interim distributions and dividends … and the notional returns as those distributions are reinvested. There are various primers on IRR calculations. One can use the Hewlett Packard calculator, which will do the math for you. [1] Even more labor saving, you can take advantage of a small promotional handout (a wallet sized card) by one of the leading funds investing in secondary positions, Coller Capital. With the permission of Coller Capital, the information is reproduced here. [2]

The point is that investment pros talk IRR … the language everybody uses since the IRR calculation enables the investment business to work with 'apples to apples' comparisons. The Coller Capital "cheat sheet" enables the lay person to speak "IRR" knowledgeably, alongside the professionals.

[1] By Calculator (Hewlett Packard 12C):

Assume that you are being offered 25% of a company valued at $1,000,000 for a $75,000 equity investment. You want to evaluate your annual rate of return on that investment.

Assume you plan to exit from the deal in 5 years.

Assume that no cash payments (e.g., dividend) are paid before you exit from the deal. (Dividends would be cash flows each year).

Calculate the nominal amount of the $75,000 investment in year 5 by multiplying the percent ownership by the company's estimated value: .25 * $1,000,000 = $250,000

This means that the cash flows are as follows: -75,000 in Year 0 (before the investment makes any returns), 0 for Years 1 through 4 of the investment, and 250,000 in Year 5 when you exit from the deal.

[2] Coller Capital's cue card also matches the exit result, as a function of initial investment, with the product of compound interest:

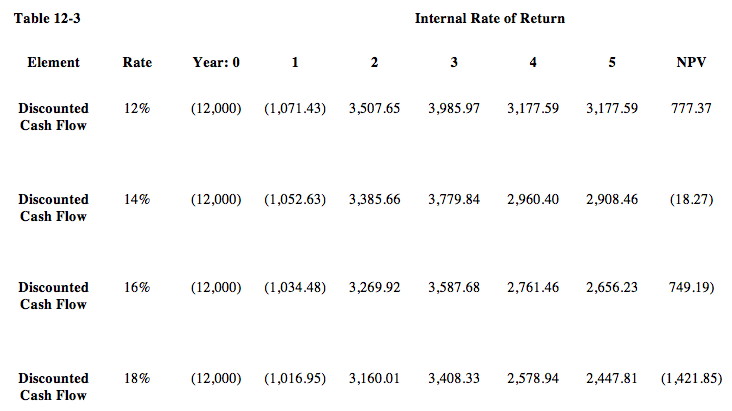

IRR is the discount factor that yields zero NPV. As is true of the NPV's shown in Table 12-3, you can see that the IRR must be slightly below 14 percent because the NPV at 14 percent is slightly less than zero. The precise IRR (12.95 percent in our example) can be calculated as with the NPV in a spreadsheet program by entering the amounts from Table 12-1. NPV and IRR decision rules are interrelated. If your target discount rate (often called the hurdle rate) had been 14 percent rather than 10 percent in Table 12-2, the NPV (-$18) and IRR (13.95 percent) would miss your goal.

081914-1